21

Mar

Working with tax deductions for student loans get a break on your tax return scholarships and delivers are high sources for college, due to the fact the cash is now not paid back. Rewards and 0% introductory apr offers make it tempting to pay off student loans with a credit card, but first, do the math.

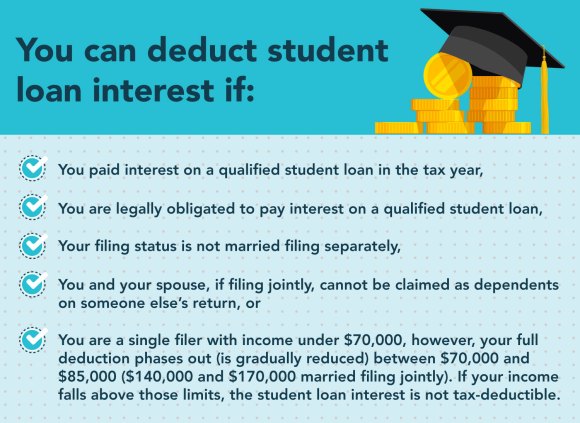

Tax deductions for paying student loans. What amount of interest can i deduct from my tax? If you made interest rate payments on your student loans during the tax year, you could deduct up to $2,500 in interest paid. For student loan interest, the maximum deduction is $2,500 for single filers, heads of households, and qualifying widows or widowers with modified adjusted gross incomes of less than $70,000.

The interest you paid on your student loan may be deducted during your tax year if you qualify for the benefit. The student loan interest deduction. If you happen to qualify for the 22% tax rate, you have the best deal because your.

Can you still deduct student loan interest in 2020? Vsac student loans that qualify for a tax deduction Under the taxpayer relief act, student loan interest is considered a tax deduction in some cases.

Working with tax deductions for student loans get a break on your tax return scholarships and delivers are high sources for college, due to the fact the cash is now not paid back. Student loan interest is interest you paid during the year on a qualified student loan. This includes capitalized interest, which is still counted as interest and is assumed to have been paid on a prorated basis.

However, if your modified adjusted gross income (magi) is less than $80,000 ($160,000 if filing a joint return), there is a special deduction allowed for paying interest on a student loan (also known as an education loan). In many cases, the interest. They are sponsored by states or state agencies, so they’re not your typical investment vehicle.

You may only earn a cap of $2,500 a return per employee, not per individual return. As of 2021, the deduction. The tax benefits of your student loan don�t end with the above credits.

You can deduct the interest portion of a student loan payment (up to $2,500 per year), but not the principal payments. Your tax deduction is limited to interest up to $2,500 or the amount of interest you actually paid, whichever amount is less. For example, if you borrow and then use the money to pay $2,000 for your tuition, your credit will equal $400:

To claim the student loan interest deduction, you must be legally obligated to make the loan payments. $2,000 tuition payment x 0.20 (20%) = $400 credit. Normally, if you have federal student loans in default (meaning you�re unable to pay what you owe on them for 270 days), your tax refunds can be taken to help cover the balance owed.

The student loan interest deduction allows you to write off up to $2,500 per year from your taxes in student loan interest payments. There are a few options for deducting student loan interest and student loan payments on your federal income tax returns, including the student loan interest deduction, qualified distributions from. One useful tax break for college graduates and their parents is the student loan interest deduction.

Rewards and 0% introductory apr offers make it tempting to pay off student loans with a credit card, but first, do the math. Student loan interest deduction generally, personal interest you pay, other than certain mortgage interest, is not deductible on your tax return. As with the american opportunity tax credit, the irs allows you to claim the lifetime learning credit even if you use a qualified student loan to pay for your tuition.

You may deduct the lesser of $2,500 or the amount of interest you actually paid during the year. Because this is a tax deduction and not a credit, it reduces. The provision will expire in five years, although experts.

And—because this deduction adjusts your actual income—if you qualify, you can claim it even if you do not itemize your deductions. To qualify, you must meet income and other eligibility guidelines. For your 2021 taxes (which you file in 2022), this deduction is worth the amount you paid in interest for your student loans, up to $2,500, which is the maximum deduction.

Student loan interest can quickly add up. That’s why the federal government introduced the student loan interest tax deduction to help ordinary students out. A deduction is also available for the interest payments you make when you start repaying your loan.

The interest paid on first or second mortgages of up to $1,000,000 can be deducted by taxpayers. 12 hours agotaxpayers who make payments on a qualified student loan may be able to get some relief if the loan they took out was only used to pay for higher education expenses. A single person can deduct $2,500 off of their student loan payments if they’re married.

That also means that they are subject to state tax rules, including maximum contribution rates, which vary from state to state. The 529 plan a 529 plan is an investment account that can be used to save for your education. Student loan interest deduction if you have started to pay back your student loans, you may be able to reduce your taxable income by up to $2,500 of the student loan interest you have paid for you, your spouse, or your dependent.

Previous post

Tax deductions for payroll